Bitcoin Mining Pool Braiins Hits 1,000 Daily Payouts On Lightning Network

Bitcoin Magazine Bitcoin Mining Pool Braiins Hits 1,000 Daily Payouts…

Post Content

Post Content

Post Content

Post Content

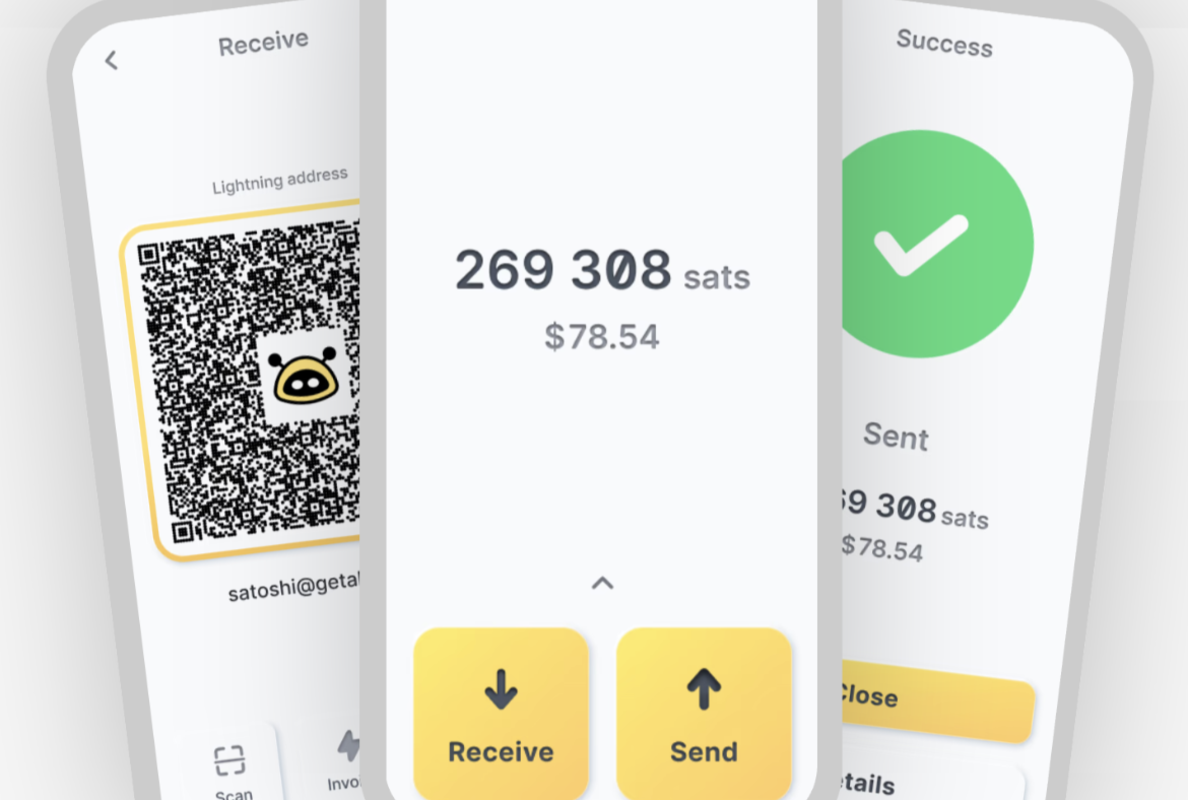

Today, Alby announced the release of Alby Go, a mobile application available for iOS and Android that allows users to make self-custodial payments via their Lightning node.

“ALBY MOBILE WEN?”

“guys, when will you release an app?”

“i want wallet from Alby on myPhone”

You can stop asking – Alby mobile is here

—————

Please welcome, on your phones, on GitHub, in your appstores…. ALBY GO pic.twitter.com/WtrJ1eKrs3

ALBY GO pic.twitter.com/WtrJ1eKrs3

— Alby  (@getAlby) September 25, 2024

(@getAlby) September 25, 2024

Users can connect the app to Lightning nodes and wallets including Alby Hub, Umbrel, Start9, LifPay and CoinOS to enable self-custodial Lightning payments. The app most easily integrates with Alby Hub, an open-source wallet that Alby recently released that makes Lightning nodes easy to access and use from multiple devices. Alby Go also provides a straightforward wallet interface to Nostr Wallet Connect (NWC)-enabled Lightning wallets.

“Alby Go is our next step in making bitcoin accessible everywhere, now bringing it to users’ pockets,” said Alby co-founder Alby Michael Bumann in a press release. “By utilizing the NWC messaging protocol, we facilitate seamless use of multiple nodes and wallets in a lightweight app.”

Other features of Alby Go include a contact list, which lets users store Lightning addresses of frequent contacts for quick and convenient transactions; currency conversion and dark/light theme settings.

Alby Go is currently in version 1.5 and Alby encourages users to contact the Alby team with suggestions on how to improve the app. The app’s code is open-source and ready for reviews and contributions.

For more information on Alby, see our Founders piece on Alby co-founder Michael Bumann.

PayPal Holdings, Inc. (NASDAQ: PYPL) has enabled its U.S. business account holders to buy, hold, and sell cryptocurrency supported on its platform, such as Bitcoin, directly from their PayPal accounts. While this service is available nationwide, it will not be available in New York State at launch, PayPal stated.

JUST IN: PayPal now enables business accounts to buy, hold and sell #Bitcoin and crypto. pic.twitter.com/mIujzhrtiF

— Bitcoin Magazine (@BitcoinMagazine) September 25, 2024

“Since we launched the ability for PayPal and Venmo consumers to buy, sell, and hold cryptocurrency in their wallets, we have learned a lot about how they want to use their cryptocurrency,” said Jose Fernandez da Ponte, Senior Vice President of Blockchain, Cryptocurrency, and Digital Currencies at PayPal. “Business owners have increasingly expressed a desire for the same cryptocurrency capabilities available to consumers. We’re excited to meet that demand by delivering this new offering, empowering them to engage with digital currencies effortlessly.”

In addition to buying and selling, U.S. merchants can now externally transfer cryptocurrency to third-party wallets. This new functionality further increases the flexibility of crypto transactions for businesses.

PayPal’s expansion into offering businesses the ability to buy and hold Bitcoin and crypto on its platform builds on its growing digital currency initiatives. This includes the launch of consumer crypto services in 2020 and the introduction of its U.S. dollar-backed stablecoin, PayPal USD (PYUSD), in 2023.

Post Content

Mircea Popsecu is a mostly forgotten figure in this space, but he was once a very impactful cultural figure early on before he slowly faded out of the wider public sphere to eventually “accidentally” drown off the coast of Costa Rica. He was quite an insane and eccentric figure, but he has left a lasting impact on this space. I would argue he is essentially the Godfather of what people these days consider “toxic maximalism,” although compared to people who claim that label today he would make them seem like overly sensitive and whiny children.

One of his most prolific posts in my mind was his consideration of the price of Bitcoin and the market dynamics that entails in the long term, from 2013. He was discussing the dynamics of supply and demand interacting with each other, and specifically the mentality of current bitcoin holders in contrast with average consumers that may or may not have an incentive to attempt to accumulate bitcoin in response to the deterioration of the fiat system.

He framed the posited friction between these two groups as an impasse, where current holder have no great incentive to part with their bitcoin, and people trying to get rid of their devaluing fiat have no real recourse if holders of bitcoin act in that way.

He proposed three possible solutions to that impasse.

“One of them is that consumers yield and submit, Bitcoin goes to somewhere in the thousand dollars per range and there’s a rush to move society away from the dysfunctional standard. Banks start taking Bitcoin deposits, Bitcoin hedge funds pop up everywhere, the FED chairman, ECB chairman and everyone else come to Timisoara whenever they want to make a move to obtain my blessing and so forth.”

This is the path we are seemingly on right now. Capitulation of the existing system, integration into the legacy financial system, the veneration of early adopters and Bitcoin as a solution to the systemic problems of fiat. This is what Bitcoiners currently cheer on in terms of our path forward, citing every tiny piece of news from a banking institution, an ETF, an investment fund, as proof that they are capitulating! We have won!

This is pure and utter delusion. Trump pandering to Bitcoiners seeking campaign financing does nothing to truly benefit Bitcoin, he is and will always be a fan of the dollar. His mentality is based around the idea of the money printer, and exporting our inflation globally, being a massively positive thing for American interests. The Democrats overwhelmingly are antagonistic towards the space, for similar reasons.

Even if such a future was to truly come to pass, in actuality and not just in name, it would be a very dire and depressing future for anyone who looks to Bitcoin as a tool for freedom and sovereignty. Using Bitcoin would provide that to almost no one. Hedge funds, banks, ETFs, would all be the keyholders for the vast majority of people. No one would truly have any degree of freedom, it would be the same financial system we exist in now where nothing can be done without seeking the permission of some overlord who truly has control of your funds. Regulations would not enable more competition in this sphere, the existing players would take advantage of their revolving doors to encourage capture and high walls around their privileged position in this role.

This path would essentially mean failure of Bitcoin as a tool for freedom, and the same game we see being played right now with slightly stricter rules for the privileged few who can get a seat at the table.

“Another one of them is that consumers revolt, governments intervene, we all spend the remainder of this decade fighting with each other. Bitcoin also goes to thousands of dollars per, but the energy, effort and resources which could have been expended on comfortably yielding and productively submitting are wasted in an ultimately doomed effort to play tough on a weak hand. Neutral and unengaged governments win, and as the dust settles the balance of macroeconomic power has shifted from the Western world to whatever, China, Iran, Brazil, what have you.”

This is the path of them fighting Bitcoin overtly. People actually start switching to Bitcoin en masse, and governments react in a reflexive manner to try to prevent this. Things domino from here as Bitcoin begins to become a more important aspect of global finance outside of the purview of the legacy financial system, and countries that fight and refuse to let it happen wind up just screwing themselves over as smaller and more adaptive jurisdictions who stay out of it or embrace this change wind up benefiting enormously.

In this world Western governments make using Bitcoin an enormously difficult task, but people persevere anyway. The rest of the world with a brain stays out of the way, or proactively embraces it, while the West spends all of its effort and resources futilely fighting the inevitable. The rest of the world experiences a financial renaissance, while the Western world stagnates, its citizens forced to fight uphill the entire time to retain any degree of economic success (or even just staying afloat).

As brutal as it sounds, this is the world I want to see. One where the West’s domination and coercive control over the rest of the world erodes. We have no special right to lord over the rest of the world in the manner we do, and this path forward would strip us slowly over time of the ability to continue doing so. Citizens of the West can embrace Bitcoin, and stand up for our individual freedoms and sovereignty, and in doing so cushion ourselves from the collapse of our corrupt institutions.

A victory in revolution doesn’t come free or easy. For Bitcoin to really do what many of us hope it can, it’s really necessary at the end of the day to walk a painful path. And that means people have to choose to walk it. Many people in this space think that governments will simply roll over and let Bitcoin win, but that is just a feint to move in and capture it.

We need to push to build around them, build in parallel, and force their hand. If they don’t actively fight it, then there is something else going on. That isn’t good for us.

“Yet another one of them is that consumers revolt, entrepreneurs intervene, before the end of 2015 there’s about a thousand to a million different Bitcoin forks, each with its ten million-ish monetary base worth about a dollar, on global average. The size of the inter-Bitcoins market, the complexity and confusion ensuing makes pretty much everything unmanageable for the “ordinary person”. Hedge funds and banks (the ones a little ahead of using Excel) that trade in this murky complexity make a killing and become the principal driver of economic growth worldwide. Not only is the consumer about as screwed as is currently the case, but to everyone’s benefit he has just been clearly proven yet again that revolt = being fucked in the ass harder, longer, with a thicker implement with sharper barbs on it. Also conveniently, the thing to revolt at has become much more vague and intangible. On the balance of probabilities this would seem the most likely outcome, strictly because history unerringly flows in that direction which most cruely rapes the “average person”.”

Popescu rated this as the most likely outcome. Constant fragmentation, Bitcoin shattering into an innumerable number of forks from the original. Each region, or group of people with a different idea, breaking off into their own different networks. Erosion of the network effect until it localizes with more sub-fragments than people can keep track of.

Everyone assumes that this is over, that this door was simply a phase we passed through during and in the immediate aftermath of the blocksize wars, and it is closed forever. That is delusional. Nation states are adopting Bitcoin, major financial institutions that essentially write government policy are stepping on stage and integrating it into their systems.

The world is a game of coercion and extortion politics, the US invades countries and slaughters hundreds of thousands of people simply to keep the flow of commodities moving in the direction it wants to. To imagine they and other interests wouldn’t fork Bitcoin for their own self interest at a global scale is naive. I would even go so far as to say that opening the first door, the “capitulation” and capture of Bitcoin quickly by these people would almost guarantee that this last door eventually opens.

This is a failure of the utmost degree. Fragmentation, no singular network effect that enforces a true scarcity of supply, and more importantly rules, on economic players globally. A brief respite and then immediate return to the game we know now. Complete and utter failure of any form of revolution.

All three of these doors are still sitting there, we haven’t walked through any of them yet. It’s anyone’s guess which one we eventually do. Bitcoiners could do with a little humility, and recognition of the fact that not only have we not even come close to winning, but failure is absolutely still on the table. In multiple ways.

A few days ago, a new initiative promoted by Prime Minister Netanyahu was announced – removing 200 shekel bills from circulation, as a first step to abolish cash altogether within a few years.

The official excuse? fighting financial crimes and black money in the Arab society.

As expected, this move – identical to India’s move in 2016 – will cause further destabilisation of Israel’s economy and of its citizens’ physical and mental states. A derivative of this economical shake up will ripple into Gaza who is relying on the Israeli shekel as its currency, and clearly, its population is heavily reliant on cash.

So let’s break it down.

The value of the Israeli 200 shekel bills surpasses 100 billion shekels, and make up nearly 80% of the bank notes held by the public. In recent attempts to smear cash holders, it was reported that “most of the 200 shekel bills are not used for purchases, but for the accumulation of black capital.” A team of so called experts: nine businessmen and former officials in the public sector, who initiated the idea to abolish these bills, claim that the bills’ removal will recover more than 20 billion shekels ($5.3b) by next year, and 110 billion shekels ($29b) in the next 5 years – bringing it back to the state, and will force tax evaders to be revealed.

Two weeks ago, the first mainstream media article about this new initiative popped up, to normalize and prepare people for this draconian measure.

Removing the 200 shekel bills from circulation, as well as broadening the obligation to report on cash holding to the authorities. This is part of a larger plan to abolish cash completely in 3 phases: 1- limit cash transactions to 3,000 shekels ($800) within 2-3 years, 2- lower transaction amount to 2,000 shekels ($530), 3- cancel cash usage completely, while encouraging digital payment methods.Leveraging AI tools for monitoring and enforcing tax evasion,Launching a collaborative enforcement effort that includes various key bodies, such as the Tax Authority, the Anti-Money Laundering Authority, the police, the prosecutor’s office and the Counter-Terrorism Economic Warfare Headquarters.Banning the possession of cash substitutes, such as gold, silver, medals, and coins, on a significant scale.Enhancing regulation of non-banking financial entities, including currency exchange services, which manage significant volumes of illicit funds.Seizure of digital currencies linked to terrorist activities of sanctioned entities – “There are technologies that enable the real-time identification of such money transfers, and Israel needs to implement them immediately. This will allow for disrupting the flow of funds for terrorism and crime, identifying terrorist operatives, and seizing hundreds of millions of dollars for the state, potentially billions in the future”. (This part is from a leaked draft of the plan dated March 2024; it did not appear in mainstream media publications – E.F)

Lo and behold, two weeks after the first “suggestion” of this new policy, Prime Minister Netanyahu announced he’s now advancing this reform urgently in order to fight black capital, especially amongst the Arab population, and called in a special committee to discuss the new policy.

Israel already introduced a new “big brother” regulation last year, for pre-approving any B2B transaction with the Tax Authority, over 25K shekels. The new policy plan now proposes lowering the threshold for transactions requiring pre-approval from the Tax Authority from 25K shekels ($6,750) to 5K shekels ($1,350), a highly controversial move.

Israel’s largest mainstream publication, Ynet, reminded its readers that “Similar steps have been implemented in other countries. In parts of China, the use of cash has been completely banned in certain cities.” Israel’s governing bodies love using “other countries are doing it already too” excuse to justify their acts. The same mantra is being played again and again when the Digital Shekel is mentioned. I recently listened to a podcast with Israel’s Central Bank governor which mentioned favorably how advanced the ECB is with the Digital Euro, for example.

• Israel’s is promoting an initiative to abolish the 200 shekel bank notes as a first step to narrow use of & abolishing cash. Same as in India in 2016.

• Physical gold & silver may be forbidden to hold.

• Gaza’s population suffering from financial oppression via lower… pic.twitter.com/XUbCUKDgFE

— Efrat Fenigson (@efenigson) September 22, 2024

My video on the new 200 bills plan went viral with 70K views, share it here

In November 2016, the Indian government made a similar decision to the one Israel is now considering, by withdrawing 500 and 1000 Rupee notes from circulation. In the aftermath of this decision, hundreds of people lost their lives, many more faced hardship, and the country’s GDP took a significant hit.

Read this on BBC hereRead this article here

From this 2016 article on Vox:

“Tens of thousands of people have taken to the streets of cities throughout India to protest an economic policy you probably haven’t heard of before: demonetization.

Three weeks ago, Indian Prime Minister Narendra Modi surprised his country with an announcement banning 500- and 1,000-rupee notes — worth about $7 and $15 respectively — in a bid to tackle corruption and terrorism.

He estimated that forcing people to exchange the country’s largest currency bills for new banknotes would allow the government to crack down on “black money” — unaccounted-for cash holdings that haven’t been taxed but, under the law, should be. He also argued that it would strike at domestic terrorist financing operations by capturing counterfeit money and rendering the legitimate cash they kept in the shadows worthless.

Banning widely used banknotes would have a huge impact on any economy, but in India the policy is transformative. Modi’s sudden ban instantly meant that 86 percent of all the cash in circulation in India was no longer considered legal tender, which means that businesses could refuse to accept those bills as a form of payment. And the Indian economy simply runs on cash: It’s estimated that between 90 and 98 percent of all transactions in India, measured in terms of volume, involve it.

Unsurprisingly, Modi’s demonetization initiative has caused chaos across the country. People want new banknotes, but the current supply of them isn’t close to meeting demand. That’s created headaches for people as they wait in long lines outside ATMs and banks, which routinely run out of cash. For people who rely on daily cash earnings to survive, it can mean not being able to obtain food.”

In this excellent lecture by Andreas Antonopoulos, a famous Bitcoin developer and lecturer, dating back to 2016, Andreas discusses the currency war of countries. He details the cash crisis in India and other examples of countries where citizens are punished due to failed currencies (Venezuela, Argentina, Ukraine, Turkey and more).

All of these trials conducted in one country, serve as testing grounds for future implementations elsewhere (such as the 2012 bank deposit confiscations in Cyprus or efforts to protect banks from collapse in the U.S. over the years). As debt continues to rise, the economic situation deteriorates, and inflation worsens, these experiments will only speed up. We can expect more taxes, further restrictions on cash, more confiscations, and rising prices alongside inflation. Eventually, this deteriorating state will provide a sufficient justification to introduce a new digital control system known as the CBDC, if another “crisis” or “emergency” doesn’t precede it.

Israel’s government has been tightening its policy on cash usage in recent years; Today, there are still no official restrictions on the amount of cash that can be kept at home, but the government has repeatedly emphasized that it does not view this practice favorably and prefers that as many transactions as possible be conducted through non-cash payment and money management methods. At the same time, the government is working to advance legislation that would make it illegal to hold more than 200,000 shekels in cash. Additionally, holding cash amounts of 50,000 shekels or more would require providing explanations to the authorities about the source of the money and its intended use.

In August 2022, Israel announced it forbids cash purchases larger than 6,000 shekels. This reform aims, according to a statement issued by Israel’s Tax Authority, to fight organized crime, money laundering and tax non-compliance.

The Jerusalem Post reported back in 2022:

Under the new law, any payment to a business above 6,000 NIS ($1,700) must be made using alternative methods, such as a digital transfer or a debit card. Trading between private citizens who are not listed as business owners will be limited to 15,000 NIS ($4,360) in cash. This is another step in Israel’s fight against the use of cash. Previously, cash up to the amount of 11,000 NIS ($3,200) could be used in business deals.

“We want the public to reduce the use of cash money,” adv. Tamar Bracha, who is in charge of executing the law on behalf of Israel’s Tax Authority, told The Media Line. “The goal is to reduce cash fluidity in the market, mainly because crime organizations tend to rely on cash. By limiting the use of it, criminal activity is much harder to carry out.”

“The goal is to reduce cash fluidity in the market, mainly because crime organizations tend to rely on cash” — Adv. Tamar Bracha, Israel’s Tax Authority, 2022

The cash shortage in Gaza has intensified the already dire conditions, making it even harder for people to buy essential food and supplies.

In Gaza, the scarcity isn’t limited to food, water, and electricity. Almost a year into the conflict, there’s a severe shortage of cash. Banks have been destroyed, and frequent power outages have rendered ATMs inoperable. Reports from the region highlight how this lack of cash is worsening the daily struggle for survival, while raids by the IDF on Hamas outposts have uncovered millions of shekels and large sums of U.S. dollars stored there.

Credit: Ynet

Cleaning with soap and water and returning to customers: Gaza’s worn banknote crisis

As reported on Ynet:

“A shortage of fresh cash and the closure of many bank branches due to the war have forced Gaza’s residents to reuse the same banknotes for almost a year. “With so much use, the notes become worn and decayed, and I refuse to accept them,” says one market vendor. Meanwhile, a new profession is emerging in the strip: cleaning and refurbishing worn banknotes.

The closure of numerous bank branches in Gaza since the beginning of the war has led to a severe cash shortage, forcing residents to continue using old, tattered notes. A new trade called “note cleaning” is emerging, where old bills are cleaned and restored for reuse, with the service costing between 2 and 5 shekels per note.

Merchants, particularly in northern Gaza, warn that the only real solution to this crisis is reopening the closed banks and injecting fresh cash into the market. Otherwise, the risk of counterfeit currency spreading grows.

Additionally, cash withdrawals from ATMs in Gaza come with hefty fees ranging from 10% to 20%. Before the war, there were around 20 currency exchange offices in Gaza City alone, run by Hamas or taxed by the organization. These offices traded in various currencies and converted them, alongside several informal money changers operating in market corners.”

Israel going cashless is another step in tightening control and violating property rights, for its citizens and its neighbors. This “going cashless” development is added to other worrying trends in Israel such as chewing on people’s pensions, and progressing Israel’s CBDC, the Digital Shekel.

A new economic reality is ahead of us. In such times, learning about Bitcoin becomes a necessity, in order to hedge against government tyranny with the only truly decentralized, secure cryptocurrency which is controlled by no one, and is fully permissionless, outside of government control.

This is a guest post by Efrat Fenigson. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Post Content