Jason “Spaceboi” Lowery’s Bitcoin “Thesis” Is Incoherent Gibberish

Jason Lowery’s Softwar “thesis” is a complete joke. It is…

We all have a journey to Bitcoin. Some started as sound money advocates who adored Austrian economics and gold. Others fell out of the TradFi world when they knew something wasn’t quite right. Most Bitcoiners have gone through trials and tribulations of altcoin hell. However you made it here and to Bitcoin, welcome–and buckle the F*ck up.

When I first became interested in Bitcoin, it was July of 2017, and it was already well into the bull market of that year. I bought some and watched its value increase. Then I bought more. As tends to happen during these parabolic bull runs, I kept watching the price rise and my interest go from:

Interested to Disbelief to Infatuation to Degenerate Buying to Despair.

This is a trajectory you can avoid during the next bull run if you prepare yourself properly.

If you are reading this hoping to find all the answers, I have some unfortunate news. There are no right answers in Bitcoin or life. We are all on a journey to figure out what to do and how to approach. I hope to guide you, but ultimately, your personal goals and disposition will dictate how you handle volatility. Bitcoin will test your resolve.

During the later phase of the 2017 bull run, I talked about Bitcoin to everyone in my life—completely obsessed. My neighbor at the time was older than me and had experienced the dot-com boom. I will never forget the advice he gave me; this advice was born of gaining (and losing) a lot of money during the dot-com bubble. He listened to my fervent interest in Bitcoin, and he took a very measured approach to my evident LOVE for this asset. He told me that during the dot-com boom, he made more money than he ever believed he would have, and in the end, he was right back where he began—because he rode the bull market over the top and didn’t sell anything. His advice was, “I’m glad you are doing well, but don’t forget to take some profit.” He advised me to sell 50% and keep 50%—a simple hedging strategy. I did heed his advice shortly after Bitcoin hit its all-time high and sold some of my holdings near that local top.

Now, I know that this is sacrilege to many hodlers. We don’t sell our bitcoin, right?? Well, that is a personal decision, and depending on your risk tolerance and place in life, you may want to take some risk off the table. That is part of investing, and as the old saying goes, no one ever loses money selling for a profit. This article aims to give the advice I wish I had gotten when I first discovered Bitcoin. I hope this helps newcomers to the space understand how to navigate the bombastic environment that bitcoin produces during its bull runs.

I have seen two bull runs, one in 2017 and one in 2021. These bull runs were VERY different, and I suspect that if you spoke to those involved in bull runs prior to 2017, you would find that those also had a very different feel.

The first thing I want to get off my chest is this—No one knows what is going to happen:

Balaji talks about 1 million in 3 months Nobel laureates are saying it will go to zero Buffett and Munger(RIP) call it rat poison

Whoever you are listening to, no matter how long they have been in the space or how correct they have been in the past, IT DOES NOT MATTER. They have no idea what the future holds.

In investing, there is an idea called survivorship bias. Those who have been correct have survived, and they seem like geniuses because they have been correct. The VAST majority of those who have been wrong are forgotten. You don’t hear about them. I won’t throw anyone under the bus here, but there were prominent people in Bitcoin calling for MUCH higher prices when we were sitting at 68K in 2021. I’m not saying that they are bad people; I’m sure that they had a good reason to forecast these numbers, but if you had taken their advice at that time, you would have bought at the worst time possible and gotten crushed for YEARS.

In my view, there are different tiers of crystal ball holders out there, and the lowest tier is the technical analyst type. These are the dime-a-dozen people you see on Twitter spouting off about momentum, price levels, cup and handles, etc. These people were calling for 10K bitcoin when it bottomed at 16k. I’m not saying that TA is all nonsense; fundamentally, it is a system for predicting human action through probability. It’s a consideration at best. It should never be used in a vacuum to determine your allocations. If you use it in conjunction with fundamentals, it can be much more helpful. The point I am driving at here is there are GRAVEYARDS of TA analysts out there who told you to buy at 68K and not to buy at 16K. They are throwing probabilistic darts. Don’t put your financial future on someone’s educated guess.

The second brand of crystal ball aficionados out there are macro analysts. These people have more credibility in my view because they are assessing the general trend in the economy. They are considering interest rates, Fed movements, and economic data. These types are MUCH closer to base reality because they have their finger on the pulse of the economic heartbeat. But, as with TA analysts, these people can be TOTALLY wrong. Many said that Fed funds rates couldn’t exceed x or y, or the entire economy would collapse. Well, the interest rates have been elevated to levels well above their doomsday predictions, and we have not seen a collapse.

Whether you follow a TA analyst or a Macro analyst, they can be utterly WRONG because of a black swan. Nicholas Taleb—famously hated by Bitcoiners—coined the phrase black swan to label events that happen from time to time that simply cannot be predicted in standard modeling because they are so unlikely. Covid was a black swan. The war in Ukraine was a black swan. And guess what, there could be another unpredictable black swan tomorrow that could render all of the TA and macro analysts completely wrong. The world has a ton of randomness. By the way, black swans aren’t always bad. They are just as likely to be positive catalysts.

So does this mean we should remain paralyzed with fear and not trust anyone??

Absolutely not. It means we should make the effort to EDUCATE OURSELVES! You need to take responsibility for yourself and your decisions. You can take the information from the TA analysts and the macro analyst and make your own educated decisions. THIS IS OF THE UTMOST IMPORTANCE.

Bitcoin is an incredibly simple yet endlessly complex animal. Your education will never be complete, but you can incrementally expand your understanding. We did a 10-episode Bitcoin Basics Series with Dazbea and Seb Bunney, and I don’t feel like we even scratched the surface!

You want to be educated for resiliency. If you have a solid grasp of Bitcoin and how it works, you will not be easily shaken. The psychology here is VERY IMPORTANT. If you understand what you are investing in, and the market is hit by an exchange failure similar to what happened to FTX, you will understand a few things that the average person may not.

Bitcoin is unaffected The price drop is temporary and without merit Therefore, this is a great time to be accumulating Bitcoin

Now, the opposite of this is also true. When you see mainstream headlines fawning over Bitcoin, with the gains never seeming to end, and you feel like you should drop every bit of money into Bitcoin because its price is going nowhere but up—BE CAUTIOUS. I have found that my psychology is typical. I have fear when the price is getting crushed, and I have irrational exuberance when the price is rising quickly. If I do EXACTLY the opposite of what my monkey brain tells me, I find I’m often doing the right thing. That is to say, when you feel extreme fear, this is the time to buy, and when you feel elated, this is the time to sell.

Panic buying is dangerous. When you feel an uncontrollable urge to buy Bitcoin, take a deep breath. I can assure you that you will be able to buy some, and if you are feeling the urge this strongly, the market is probably ripe for a pullback. That is no guarantee, but in my experience, this has been the likely case. I am not advocating for trading BTC, not at all. I can honestly say that I have lost more BTC than I have gained by trading, and if most people are honest, they will admit the same. Trading is a skill and discipline that very few people master.

The typical psychological roadblocks that hang people up are fear and greed. Reflect on your feelings and recognize when you are experiencing these emotions. They will cause you to make mistakes. The simplest way to mitigate all of this is simply to dollar-cost average. Swan is the PERFECT place for DCA. Dollar-cost averaging takes all the stress out. Full stop. If you level into this asset at this moment and it drops to 30% overnight, ask yourself honestly: Do I have the stomach for that? Do I have the conviction for that? Do I have the educational chops to understand why the dollar price doesn’t matter in the short term? Will I panic sell? If you aren’t convicted, dollar-cost averaging will save you. You are getting the average price over a long period of time.

I have a little DCA tactic that is simple and works for me:

When the price corrects I increase my DCA, when the price gets frothy, I feather back and average in with less. Over months and years, this supercharges your average buy.

Have a plan and be ready to execute. My neighbor’s plan is a solid place to start. Once you have doubled your money, take the initial investment out. There is a significant asterisk involved in this—What are you going to buy instead of Bitcoin? Inflating cash? The choices for where else you put your money these days are very limited. This might be controversial to many in the space, but I think it’s perfectly reasonable to sell some Bitcoin. If you have been holding for YEARS, and your stack could meaningfully make your life better, by all means, sell a portion.

Time is the one asset that is more valuable than BTC; we have a truly finite amount of time on this earth. If you hodl your BTC and then take a dirt nap, what was the point? If you can sell a portion of your stack and pay off your house, or get out of crushing debt, I think that is a sound decision. It may not be the BEST financial decision, especially if your house is on a low-interest rate loan, but it’s an understandable decision because of the peace of mind this could bring. However, you must also remember that selling Bitcoin will very likely be a painful decision in the long term.

Selling Bitcoin for toys on the other hand is not a great move. When you buy that 250k moon Lamborghini, which loses 50% of its value in 3 years while Bitcoin has gained more than that percentage to the upside, the regret will be unbearable. Robert Kiyosaki comes to mind. His book Rich Dad Poor Dad has been very influential on me, and his description of assets vs. liabilities hit home:

An asset generates cash flow A liability subtracts cash flow

If you buy assets, your net worth will increase substantially on an exponential curve. If you are buying liabilities, you are simply getting poorer. If you sell Bitcoin, you will likely regret it in the long term.

Time preference is a topic often visited in Bitcoin. Having a low time preference means you are willing to forgo niceties today for a better future. Every worthwhile cathedral, every classic piece of art, everything beautiful in this world has been built because people worked with an eye to the future, not the present. If DaVinci taped bananas to the wall we would have never remembered him. If the great pyramids had been built of clay, they would be gone. If Civilization spent all of its wealth on the here and now without investing in the future it would not last.

Bitcoin itself is a digital artifact that has been crafted to perfection by a mysterious architect. It is designed to last eons; if civilization lasts, it will have perfect fidelity into the future. Because no one can change it or control it, Bitcoin is anti-entropic. This is the epitome of low-time preference craftsmanship. Bitcoin is a Da Vinci in a world of bananas taped to walls. It’s so apparent once the work is put in that it’s embarrassing more people don’t understand the value proposition.

In stark contrast to this Bitcoin masterpiece, we have the sand hills we call alt-coins or shitcoins. These have been built using Bitcoin’s technology but introducing entropy. Fidelity is lost in altcoins because each has a founder or group who controls them. When humans can control something, they inevitably manipulate it to their benefit. And whether consciously or subconsciously, it will degrade. Most of these shitcoins have been designed from the outset to scam you. Some of these alt-coins have leadership that may be well-intentioned, but they are human and capable of being influenced and coerced. The problem is LEADERSHIP. Bitcoin and its time chain have been designed to remove the human element as a primary characteristic. Introducing humans into the mix causes entropy to destroy value through seigniorage.

Bitcoin’s invention was that of NON-INTERVENTION by humans.

These are insights that take years for many people to understand completely. If you want the TL;DR on altcoins, it’s simple. Just don’t bother. You are better off taking your money to a casino and playing craps. The deck is stacked heavily against you in the crypto world; you are simply getting lucky if you make money. Take the low-time preference route and stack Bitcoin while learning as your investment grows. I can confidently say that you will be much further ahead in 5 years dollar-cost averaging into Bitcoin than you will be gambling on shitcoins.

Most people get interested in Bitcoin during one of its parabolic bull runs. I was one of them. We are all interested in getting ahead financially, especially with the specter of inflation hanging over our heads.

If you are new to Bitcoin and this is your first foray, make sure you are prepared to hold this asset for a minimum of 5 years. You are likely here during a bull run, and unless you got lucky, it’s probably on the trailing end of the bull run. As of the date of writing in December 2023, I believe we are at the beginning of the next bull market. With the ETF approval, the halving in April 2024, and the Fed poised to turn dovish, many catalysts are aligned. This does NOT make it inevitable. Black swans are always a possibility. With that black swan caveat aside, we seem poised for massive price appreciation in the next few years.

The first time you buy Bitcoin at the exchange of your choice, it will feel like buying any other asset at a brokerage. You buy Bitcoin, and the number on the screen reflects the amount of bitcoin you now “own.”

It is critically important that you take custody of your Bitcoin. We have seen exchange failure and downright fraud go on very recently. When these frauds are uncovered and prosecuted and the price of Bitcoin gets hammered because many people associate the asset Bitcoin with the exchanges that sell it, this becomes a HUGE buying opportunity. When FTX failed 1 year ago, the price of Bitcoin was negatively affected, and those who understood that Bitcoin had no fundamental problem loaded up. They understood that fear was coursing its way through the market (back to why being educated is SO IMPORTANT in this space). If you bought Bitcoin at that time (around 16k), you secured well over a 100% gain in a year!

Think of seed keys as the password to your Bitcoin, which must be protected because if anyone else gets it, they can take possession of your Bitcoin—no bueno. Bitcoin Seed keys are generally protected by a hardware wallet or signing device. This device protects your seed keys from hackers or bad actors. I have been using Coldcards for years, and they are some of the best devices for protecting seed keys. It works very simply. You create your secret keys using the device; it saves them and keeps them offline, never connected to the internet. That last point is IMPORTANT. You do not EVER want to save these words on an internet-connected computer. The only place to safely store your Seed Keys is on a device designed for them. If the computer is compromised (and believe me, it is VERY LIKELY COMPROMISED) the signing device will protect your Bitcoin.

This may all sound very difficult and complex if you have never done it before, but trust me, it’s easy. I would recommend that you watch BTC Sessions videos about using the signing device you choose. He has incredible walk-through videos on YouTube that explain how to do everything in detail.

Collaborative custody with a company like Swan Bitcoin or Unchained Capital is also a good idea for those new to the space. They will hold your hand and protect you from making simple mistakes that can cause issues. Collaborative custody is worth the cost if you are worried about losing your Bitcoin. Unchained offers a collaborative custody product that can hold multiple keys and can help your relatives retrieve your Bitcoin in the case of your demise.

DO NOT BRAG ABOUT YOUR BITCOIN. There is a temptation to brag about success. If you stay the course for five years, you will likely have it. You are proud that you have had the discipline and self-control to master yourself and successfully acquire what you view as a significant amount of Bitcoin. Don’t share how much you have with others. This should be obvious, but there are people that may not be so excited for you. They may tell their friends, and sooner or later someone who you don’t know, who may have the capacity for violence, may decide you are an appetizing target. This is yet another reason to use a multi-sig setup. Even if someone obtained 1 of 3 keys, they cannot steal your Bitcoin.

Don’t purchase the shiny new ETF Wall Street is offering. Buy Bitcoin only at places that allow you to take actual custody of your Bitcoin. Don’t put your Bitcoin on any kind of service that offers a yield, especially if that yield seems unrealistically high. As a general rule of thumb, just don’t do it.

The first and most important reason you should take custody of your Bitcoin is that you have absolute and complete control of it. There is a saying in Bitcoin, “not your keys, not your coins.” If you do not have custody of your Bitcoin, you simply have an IOU. This is the entire reason for Bitcoin’s existence. To remove middlemen and allow people to control their financial destiny.

When you have custody, you do not incur a fee like you would with an ETF. These fees can seem low, but over time they can be SIGNIFICANT. GBTC is a trust that is the most similar to a Bitcoin ETF. GBTC charges a 2% fee PER YEAR (now 1.5% with the ETF). Over time this can be significant. Additionally, the ETF products that Wall Street is selling don’t allow you to EVER custody the bitcoin. An ETF could make sense for some people in some scenarios, but for anyone who can confidently build a Lego set, taking custody of Bitcoin is of similar complexity. Just do it yourself.

As Bitcoin becomes more mainstream, it will be possible to use it as collateral. Yes, I understand that using your Bitcoin as collateral takes it out of your possession and requires trust in a 3rd party. This is another case where you should educate yourself and be SURE that you have chosen a lender that is trustworthy and will not go bust. Always defer to self-custody if in any doubt.

Borrowing against your Bitcoin is impossible if you don’t have custody of it yourself. You cannot lend the Bitcoin that Blackrock is holding on your behalf. This is significant. There are tax benefits from borrowing against Bitcoin instead of selling it. If you don’t control your Bitcoin, you are boxing yourself out of some predictable use cases in the near future and many unpredictable uses that have yet to be invented. Programmable money is not useful if you don’t have custody of it.

The final reason you should hold your Bitcoin is a bit darker. Bitcoin was designed to be uncensorable and unconfiscatable. When it becomes apparent to the state that it is losing control of the money, it will likely come for yours. This has precedent in U.S. history. In 1933, Executive Order 6102 made it illegal to own gold for U.S. citizens. They compelled people to turn in gold and receive $20 per ounce. The government then repriced gold at $35 per ounce. You could get jailed for owning gold coins in the U.S. from 1933 until the mid-1970s. This could happen again, and you have optionality if you hold Bitcoin yourself. Custodians WILL be compelled to give the government your Bitcoin in this scenario. What you do with your Bitcoin in this situation should be YOUR call, not a custodian’s.

If you take the steps to self-custody your bitcoin, you are responsible. This is a type of radical responsibility that can worry people. If you lose your seed keys, your Bitcoin is lost forever. There is no number to call, and no one who can help you. IT. IS. GONE.

In 2017, one of my friends at the firehouse lost what was then $1300 worth of bitcoin because he put the Bitcoin on a paper wallet. These aren’t used anymore because they are so insecure, but you can print out a QR code that will hold your bitcoin. He left the piece of paper in his car. He then cleaned out his car and vacuumed up the paper wallet. That Bitcoin is gone forever. It is now worth somewhere in the range of 4-5 thousand dollars, and it’s just gone. Well, it’s technically not gone, it’s still there; just not accessible to anyone. Without the password, no one can move the bitcoin, so it’s effectively bitcoin that is frozen forever.

Another good friend of mine lost a significant amount of Bitcoin at a company called BlockFi. This was an exchange that offered yield on Bitcoin kept at their exchange. That Bitcoin is not frozen, but it is now locked up in litigation for the foreseeable future. To add insult to injury—because the Bitcoin when held by BlockFi was not technically his, it is theirs based on the “agreement” he signed when opening the account, he will at some future date get the dollar value of that bitcoin at the price when BlockFi went bust—which is 16 thousand dollars—we have rounded squarely back to why you should take self-custody seriously!

The old saying in bitcoin is “Not your keys, not your Coins.”

Bitcoin is an endless learning journey. If you want a rabbit hole to explore, you are in luck! The amount of solid content offered in the space is light-years better than in 2017. You can go from zero to proficient in a fraction of the time it would have taken back then. As was alluded to above a couple times, we have curated a Basics Series at Blue Collar Bitcoin that you can use to get started. The list of great content creators and resources is so long that we can’t name them all. Just go exploring and be careful to verify, not trust.

Continue learning, and above all—think for yourself!

Remember the wisdom of Matt Odell: “Stay humble and stack Sats.”

This is a guest post by Josh. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Get ready, brace yourself. Reading this might enrage and confound you, it might confuse you, you might even get mad enough to punch your screen (don’t do that.) Consider this a trigger warning.

Bitcoin is a database. Period. That is what it is. The blockchain is a database for storing past updates to be able to reproduce the current state of that database, the UTXO set. The entire Bitcoin protocol is built around the database. What is a valid entry in that database, and what is not a valid database entry? Who is allowed to propose entries to that database, how do you ensure that only those users’ entries will be considered and accepted? What is the authentication mechanism restricting writing entries to this database? How do you throttle database entries so that people can’t make so many it overloads or crashes the software managing the database? How do you ensure that people can’t make single entries that are large enough to cause other denial of service concerns?

It’s all about the database.

Proof-of-work? The entire purpose of that in the protocol is to manage who can actually process updates to the database. Bitcoin is meant to be a decentralized system, so it needed a way for the database to be updated in a decentralized way while still allowing users to come to consensus with all their individual copies of the database on a single update to it. If everyone is just updating their own copy of the database by themselves, there is no way everyone will come to consensus on a single version of the database. If you depend on some authority figures to handle updates, then the update process is not truly decentralized. This was the point of POW, to allow anyone to process an update, but not without incurring a verifiable cost in doing so.

Proof-of-work is simply a decentralized mechanism for updating a database.

The entire peer-to-peer network architecture? It exists solely to propagate proposed database update entries (transactions), and finalized database updates (blocks). Nodes verifying transactions as they enter their mempool? It’s to pre-filter proposed entry updates to the database and ensure they are valid. Nodes verifying that a block meets the required difficulty target? It’s to pre-filter a proposed database update and ensure it’s valid before passing it on to other nodes to update their local copy.

The peer-to-peer network exists purely to reconcile multiple copies of the same database.

Bitcoin script? It literally exists for the sole purpose of functioning as an authorization mechanism for entries in the database. In order to delete an existing entry in the current database state, the UTXO set, a user proposing that update must provide authentication proof meeting the conditions of the script locking the existing database entry. Only existing entries, or UTXOs, can be “spent” in order to authorize the creation of new entries into the database. Miners are the only ones in the protocol allowed to create entries without meeting the condition of removing an existing one by meeting the authorization requirements set out in it’s locking script.

Bitcoin script is simply a mechanism to control and restrict who can write to the database.

Every single aspect of what Bitcoin is revolves around the core central function of maintaining a database, and ensuring that many network participants all retaining their individual copies of that database remain in sync and agree on what the current state of the database is. All of the properties that make Bitcoin valuable as a form of money, or a means of payment, are literally derived from how it functions as a database.

Many people in this space think that this database should be used solely for a means of payment, or a form of money, and I empathize with that view. I too think that is the most important use case for it, and I think that every effort should be taken in order to scale that particular use case as much as possible without sacrificing the sovereignty and security of being able to directly interact with that database yourself.

But it is still just a database when you boil down to the objective reality of what Bitcoin is. People willing to pay the costs denominated in satoshis to write an entry that is considered valid under the rules of that database can do so. There is nothing you can do in order to stop them short of changing what is considered a valid entry in that database, which entails convincing everyone else to also adopt a new ruleset regarding what is a valid entry.

People can freely compete within the consensus rules to write whatever they want to this database, as long as they pay the costs required of the rules and incentive structure of mining to do so. Period. Are many of the things people can and are entering into the database stupid? Yes. Of course they are. The internet is littered with mind numbing amounts of stupid things in siloed databases all over the place. Why is that? Because people are willing to pay the cost to put stupid things in a database.

Whether that is users of the database paying the provider and operator, or the operator themselves allowing certain things to be entered as part of operations without passing the cost to a user, is irrelevant. These stupid things only exist somewhere in digital form because in some way, the cost is paid to do so.

Bitcoin is fundamentally no different from any other database in that regard. The only difference is that there is no singular owner or gatekeeper dictating what is allowed or not. Every owner of a copy of the Bitcoin database is capable of allowing or not allowing whatever they want; the problem is if they choose to refuse something that everyone else finds acceptable, they fall out of consensus with everyone else. Their local database is no longer in sync with the global virtual database that everyone else is following and using.

If you find certain database entries unacceptable, then by all means change the rules your local copy validates new entries against. But that is cutting off your nose to spite your face. At the end of the day Bitcoin runs on one simple axiom: pay to play. If people pay the fee, they get to play. That’s just how it works.

At the end of the day, it is entirely up to every individual what they want to allow or not allow in their database, but cutting through all the semantics and philosophical debates going on right now one thing remains unquestionably and objectively true: Bitcoin is a database.

Vanguard, a major player in the investment management industry with over $7 trillion in assets, has taken a surprising stance by blocking customer access to Spot Bitcoin Exchange-Traded Funds (ETFs), according to multiple reports. The move comes as a notable deviation from the growing trend of institutional interest and adoption of Bitcoin-related financial products.

Vanguard says it has no plans to offer spot Bitcoin ETFs or crypto related products, reported The Block. The firm citied that the high volatility nature of Bitcoin goes against the company’s goal of helping investors get ‘real returns’ over the long term.

Reports from clients are stating that while they can not purchase the newly listed spot ETFs, they can however sell shares of GBTC, Grayscale’s spot Bitcoin ETF. One client reportedly spoke with a company representative, who stated, “Currently we aren’t allowing those to be purchased as it doesn’t fit with Vanguard’s investment philosophy.”

Vanguard’s decision to restrict customer access comes just a day after the SEC approved spot Bitcoin ETFs for the first time, which have seen over $2.3 billion in trading volume on launch day. It remains to be seen whether the renowned asset manager will backtrack on their stance, and allow customers to participate in the burgeoning Bitcoin market.

Have you ever looked at the stars and noticed how everything in the universe seems connected? Famous inventor and engineer, Nikola Tesla, thought that this connection is all about energy, how often things vibrate, and the way they move. I believe that as well; our perceptions of every aspect of life can be perceived as a transfer of energy, a simple equation. Let’s take a moment to view the seemingly random interactions in the world as their own version of an energy transaction. The following analogies are different ways to help us think about energy, especially how we use it and share it while also respecting nature’s wisdom. Then, of course, we’ll circle back to how this all relates to understanding how Bitcoin fits into… dare I say “fixes”… this.

Focusing on the internal, energy flows in numerous ways. To have the requisite energy to win the day, I must feed my body a necessary amount of nutrients. Calories are literally a unit of energy in food. I’ve learned a lot recently about the benefits of eating quality proteins (like steak & eggs) as well as the negatives of processed foods, seed oils, etc. The quality of this energy informs the quality of my thoughts and words because we are what we eat, which directly affects my level of inflammation as well as my emotional state. If I don’t charge my battery through quality sleep, I won’t have enough energy to get through the day. My grandfather always said “early to bed and early to rise makes a young man healthy, wealthy, and wise.” It’s hard not to see all of those positive attributes as a result of maintaining the storage of energy.

In my personal interactions throughout the day, I’ve come to the point in my life where I can visualize each connection as a transfer of energy. I see my morning embrace with my wife and kids as a synergistic energy builder; we each walk away more emotionally charged because of it. As I teach throughout the day, I need to keep my energy up in order to be the catalyst, energizing my students’ neural networks through the transmission of knowledge and learning.

Listening to music that resonates within me over my lunch break helps get me pumped up. Commiserating with my coworkers sends ripples of energy, building bridges of understanding and empathy, which help us power through the day. Of course I need my dopamine fix from social media while walking the halls. These tiny sparks of energy from plebs miles away connect us while simultaneously amplifying their message. It could be said that improving our social lives is an attempt to integrate the flow of energy.

Thinking more globally, we’ve learned to harness natural forces and resources and have channeled that energy to improve our living standards. From fire to water to sunlight to oil, we’ve understood the rhythmic patterns of seasons. While respecting nature’s balance, we can see the continuous and harmonious exchange of life-giving forces within our world. We’ve been able to conceptualize a method, admittedly flawed, of transmitting abstract value in the current, traditional form of money. The economy has the potential to be buzzing with activity while sparking growth and innovation in a dynamic cycle of financial exchange. Even governments redirect energy in the form of taxes and imposed morals, shaping our world in profound ways. In politics and power, every decision and policy is like a switch that redirects societal energy, influencing public opinion and behavior, a veritable tug of war over public perception. In this light, society’s goal is to iterate towards fairness of sharing energy.

But if those analogies are valid, then how does Bitcoin fit into the concept of energy? Consider the following… Bitcoin integrates the flow of energy, maintains the storage of energy, and promotes the fairness of sharing energy.

Imagine a river flowing smoothly, finding the easiest path downhill. Bitcoin, with its decentralized nature, acts like this river, finding the most efficient ways to transfer value and energy across the globe, bypassing traditional financial dams and obstacles. But here’s the interesting part – the energy used in the mining process is not wasted. In fact, it is harnessed and put to good use. Miners often set up their operations in areas with abundant and cheap energy sources, such as hydroelectric power plants or capturing flare gas emissions. This means that the energy used to mine bitcoins is clean and sustainable, reducing the carbon footprint associated with traditional mining operations.

Just like a battery stores energy, Bitcoin’s limited supply and digital nature make it a reservoir for storing economic energy. Its value, derived from the energy expended in mining and the trust of its users, allows it to hold energy over time, releasing or absorbing it as the market demands. This means that individuals and businesses can use Bitcoin as a way to store their excess energy. For example, a power company can convert excess energy into bitcoins and store them for later use, effectively turning their excess energy into a valuable asset.

In a world where financial systems often favor the powerful, Bitcoin emerges as a beacon of fairness. Its transparent and immutable ledger ensures that every transaction is recorded and open for verification, promoting a just and fair exchange of energy. In traditional energy systems, there is often a centralized authority that controls the distribution of energy. This can lead to inefficiencies and inequalities in the system. However, with Bitcoin, the decentralized nature of the network ensures that energy can be shared more fairly. Individuals can directly transact their economic energy with each other using Bitcoin, bypassing the need for intermediaries and reducing transaction costs.

Bitcoin doesn’t recognize borders, cultures, or biases. It unites the world under a single, universal protocol for energy exchange, allowing individuals from all corners of the globe to participate in a shared economic ecosystem. As we harness more renewable energy sources and improve our technological capabilities, Bitcoin stands ready to integrate these advances, evolving continuously to channel global energy flows more efficiently.

From the sun’s rays permeating our world to the electricity lighting our homes to the feeling of a warm embrace, the world can be perceived as one elaborate transfer of energy. If this is the case, shouldn’t we be embracing a technology that harnesses, democratizes, and respects the flow of energy. As we embrace the future, let’s recognize the role of Bitcoin in shaping a world where energy flows freely, stored securely, and shared justly, empowering us all in this ongoing odyssey of energy transformation.

This is a guest post by Tim Niemeyer. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

In a notable statement, BlackRock CEO Larry Fink has expressed a positive perspective on Bitcoin during an interview today with CNBC, affirming that it “is an asset that protects you.”

“I believe it goes up if the world is frightened, if the people have fearful geopolitical risks, they’re fearful of their own risks,” said Fink. “It’s no different than what gold represented over thousands of years. It is an asset class that protects you.”

Fink’s recognition of Bitcoin as a protective asset suggests helps shift the narrative surrounding the digital currency, emphasizing its role as a safeguard amid economic uncertainties. This endorsement from the head of the world’s largest asset management firm is a significant milestone for Bitcoin’s acceptance within mainstream financial circles.

“Unlike gold where we manufacture new gold, we’re almost at the ceiling of the amount of Bitcoin that can be created,” Fink continued. “What we’re trying to do is offer an instrument that can store wealth.”

The statement comes just two days after the US Securities and Exchange Commission (SEC) approved BlackRock’s, alongside 10 other asset managers, spot Bitcoin ETF. Fink’s positive sentiment further adds to the growing chorus of influential figures recognizing Bitcoin’s potential to play a protective role in an investment portfolio.

As the Bitcoin market continues to evolve, statements like these from key industry figures contribute to shaping a positive narrative around Bitcoin, potentially influencing broader market sentiments and paving the way for increased adoption.

OP_CHECKTEMPLATEVERIFY has once again become a focal point in the conversation about improvements to scale Bitcoin. This time around there are many more alternative designs for covenants being proposed, and actual concrete designs that make use of CTV as scaling solutions (Timeout Trees and Ark). The conversation has a much larger depth of concepts to take into consideration, both in terms of alternatives that could be adopted as well as concrete proposals that CTV could enable.

One narrative circulating from the camp of people against CTV is that “CTV doesn’t scale Bitcoin.” Let’s charitably interpret that to mean that CTV itself does not scale Bitcoin, things you can build with it do. Well, then that is not a coherent argument. Segregated Witness did not scale Bitcoin. CHECKLOCKTIMEVERIFY and CHECKSEQUENCEVERIFY did not scale Bitcoin. But the Lightning Network, which those three proposals enabled, do scale Bitcoin. They add a massive amount of overhead for transactional throughput to grow beyond the constraints of the blockchain itself.

Lightning literally couldn’t exist without those base layer primitives. The problem with Lightning though, is it only scales the number of transactions that can be processed. It does not in any way help improve the scalability of ownership over UTXOs, or increase the number of users who can control one. Lightning is currently not capable of doing that with its current design and the current set of consensus primitives available in Bitcoin script.

CTV can change that.

Part of the problem of Lightning’s shortcoming regarding scalability of Bitcoin ownership is that in order to open a channel, or control a UTXO, you actually have to transact on the base layer. After that Lightning can facilitate a very large number of transactions off-chain, but a user must still transact on-chain to onboard themselves to Lightning. It massively increases the number of transactions Bitcoin can process, but it does nothing at all to increase the number of people who can own bitcoin.

This is another big problem CTV can help with. Burak coined the term “virtual UTXO” for his Ark proposal, but I think this terminology is a perfect general term useful far beyond the context of Ark. A virtual UTXO is one committed to being created in the future, through mechanisms like a pre-signed transaction, but that hasn’t actually been created on-chain yet. Bitcoin does not have the blockspace for everyone to create a single UTXO at the scale of the world population, but there is definitely potential for people to have their own independent virtual UTXO if the process of committing to those can be made scalable.

Scaling the creation of commitments to vUTXOs is the problem. Right now there is no way to create them except through the use of pre-signed transactions, and this introduces a bottleneck that must be addressed. The number of vUTXOs any real UTXO can commit to is bounded by the size of the multisig set signing these transactions. To trustlessly create vUTXOs, the owner of every vUTXO must be part of the multisig key that is signing the transactions that commit to creating them, otherwise they have no guarantee that conflicting transactions will not be generated that voids their ability to claim their vUTXO if necessary. The problem of coordinating the signing of this between every member of the set introduces practical considerations that will ultimately severely limit the size any pool of vUTXOs can grow to. The only other alternative is to have some trusted party or parties sign the transactions committing to everyone’s vUTXOs, and simply trusting them to not steal those funds from the rightful owners.

CTV offers a solution to both of these problems. By being able to non-interactively commit to a set of future transactions the same way pre-signed transactions do, but without requiring every owner of the vUTXOs those transactions create to coordinate signing, it solves the coordination problem. At the same time because no one needs to interact, a single person could take the role of funding the CTV output that commits to everyone’s vUTXOs unfurling on-chain, and zero trust in that person after the funding transaction is confirmed is required. Once that real UTXO is confirmed in a block, the person who funded it has no ability to undo or double spend the future transactions it has committed to.

Keep in mind that a vUTXO can be whatever you want it to be. It can be a Lightning channel, a multisig script for cold storage, etc. CTV does what the current form of Lightning does not, it scales actual ownership of Bitcoin, not just the number of transactions it can process.

One of the other criticisms of CTV as “not scaling Bitcoin” is that by committing to future transactions you do not escape the need to put them on-chain eventually, and so therefore CTV doesn’t actually help improve scalability. I like to call this “the OP_IF fallacy.” i.e. once people start talking about CTV they forget OP_IF exists, and that scripts can actually have multiple spending conditions to choose from.

The most powerful things about Taproot are the ability to construct multisigs by just adding two public keys together and sign for them with a single aggregate signatures, and to only selectively reveal a single “IF” branch of a script that has multiple ways to be spent. Combined with CTV, this offers a very powerful way to make use of vUTXO commitments. Rather than make a chain of transactions using purely CTV, they can be constructed with the CTV spending path buried inside a taproot tree. The end of the chain of transactions are all the individual vUTXOs each participant owns, locked to that user’s public key alone. As you go backwards towards the root of the tree, each set of keys that are below any node in the tree can simply be added together and used as the Schnorr multisig key that the CTV spend path is buried under.

This means that at any point in the chain of transactions unfurling on-chain to actually turn the vUTXOs into real UTXOs where you can get every participant in an intermediate UTXO to coordinate with each other, everyone can simply cooperatively sign a transaction moving their coins where they want to go in a more efficient way than simply letting the pre-defined transaction flow unfurl all the way to morph their vUTXOs into real ones. This allows small sub groups to escape needing to actually unfurl the entire set of transactions pre-committed to on-chain, without introducing any trusted parties to rely on or weakening the security of each user’s claim to their own vUTXOs.

These two simple realities offer a massive gain in scalability for Bitcoin without compromising on individual sovereignty or security in doing so, and all we need in order to realize them is CTV.

Acknowledgements: I would like to thank everyone who participates at the Chicago Bitdevs for helping me formulate these observations in a concise way through discussion.

After FTX collapsed, scornful critics widely ridiculed Caroline Ellison’s approach to stop losses. ‘I just don’t don’t think they’re an effective risk management tool,’ she infamously told an audience during FTX’s heyday. But did she have a point?

Venturing into the crypto asset management realm presents a unique set of challenges that differ widely from the traditional fund space. In this primer piece, we will delve into the obstacles that aspiring fund managers face when launching a bitcoin sector fund and examine the key differences that exist when you step outside the world of traditional asset management.

One of the most significant challenges faced by bitcoin sector funds is the extreme volatility that exists within the cryptocurrency market. Bitcoin’s price has witnessed strong bullish surges, driving excitement among investors. However, it has also experienced strong bearish declines, leading to substantial losses for those unprepared for such price swings. Managing risk in such a dynamic environment requires sophisticated strategies, rigorous risk frameworks and assessments, and a deep understanding of market trends.

Unlike most traditional and mainstream blue chip assets, which often experience relatively stable price movements, bitcoin’s price can change meaningfully within a matter of hours. Consequently, bitcoin sector fund managers must be well-equipped to handle sudden price fluctuations to protect their investors’ capital. Traditional stop loss structures may not work to the extent expected, as the closing market order may get executed far below the preset trigger price due to orderbook slippage and rapid price movements, the proverbial “catching of a falling knife”. Using tight stop losses as a foundational risk management mechanism can be your enemy. For example, in a flash crash scenario, positions may be automatically sold at a loss even though the market reverted a few minutes (or seconds) later.

While stop losses are an alternative, they’re not an option! Options are contracts you can buy that give you the right to buy or sell a given asset at a predetermined price (i.e., the strike price) at a given time (i.e., the expiration date). An option to buy an asset is a call and an option to sell one is a put. Buying an out-of-the-money put (i.e., far below the current price) can act as a floor on your potential losses if the price collapses. Think of it as a premium paid to insure your position.

Sometimes to defend against binary result events or particularly high volatility timeframes you just have to flatten your positions and take no risk, living to fight another day in the bitcoin market. Think for example of key protocol update dates, regulatory decisions or the next Bitcoin halving; though note the market moves ahead of those events so you may have to take action beforehand.

Creating an effective risk management plan for a bitcoin sector fund may involve using various hedging techniques, product and instrument diversification (potentially across asset classes), trading venue risk scoring and risk-adjusted allocations, dynamic trade sizing, dynamic leverage settings, and employing robust analytical tools to monitor market sentiment and potential market and operational risks.

The custody of Bitcoin and other cryptocurrencies is a critical aspect that distinguishes bitcoin sector funds from their traditional counterparts. One key difference is that unlike traditional exchanges that only match orders, bitcoin exchanges do the order matching, margining, settlement, and custody of the assets. The exchange itself becomes the clearinghouse, concentrating counterparty risk as opposed to alleviating it. Decentralized exchanges come with a unique set of risks as well, from fending off miner-extracted value to being ready to move assets in case of a protocol or bridge hack.

For these reasons, safeguarding digital assets from theft or hacking requires robust security measures, including but not limited to multi-signature protocols, cold storage solutions, and risk monitoring tools. The responsibility of securely managing private keys and choosing and monitoring reliable trading venues rests entirely with the fund manager. The burden to monitor the market infrastructure itself introduces a level of technical complexity absent in traditional fund management where custody and settlement are standardized and commoditized standalone systems.

Custodial solutions for bitcoin sector funds must be carefully selected, ensuring that assets are protected against cyberattacks and insider threats. With the history of high-profile cryptocurrency exchange hacks, investors are particularly concerned about the safety of their assets; any breach in security could lead to significant financial losses and damage the reputation of the fund.

Launching a bitcoin sector fund is a thrilling endeavor that offers unprecedented opportunities for investors seeking exposure to the fast-growing cryptocurrency market. It is important, however, to understand that launching a fund is no easy feat with pitfalls going beyond the success of the trading strategy. It is no surprise that every quarter the fund closures are in the same range of fund launches.

Those entering the bitcoin sector fund space should approach it with a pioneering spirit, stay informed, and embrace the dynamic nature of this exciting emerging market. While the road may be challenging, the potential rewards for successful bitcoin sector fund managers could be astronomical.

If you’re ready to start the fund building journey, already en route, or would just like to learn more, reach out to us at advisory@satoshi.capital.

This is a guest post by Daniel Truque. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

The core of Bitcoin’s security model relies on this basic game theory—miners, armed with their digital pickaxes, are in a relentless chase for profit. And it’s this pursuit that keeps the network secure. Basic vanilla mining involves producing blocks to earn the block rewards and transaction fees, but have you ever considered that miners might have other ways to extract value from the blockchain beyond this standard mining process? Are there other avenues for profit on the blockchain where miners can leverage their unique position as validators?

In proof-of-work systems, “Miner Extractable Value” (MEV) is a term that describes the profits miners can earn by manipulating how transactions are prioritized, excluded, rearranged, or altered in the blocks they mine. However, since Ethereum’s upgrade to Ethereum 2.0, which moved the network to proof-of-stake, the concept of MEV has taken on a new name and is now referred to as “Maximal Extractable Value” in proof-of-stake systems. In this context, it’s the block proposers instead of miners—who are the validators—that have the opportunity to extract this value.

Miners (or validators in Ethereum) have a special role in these networks confirming transactions in blocks. Their position places them a step ahead of other users and allows them to determine the final order of transactions in the chain. Inside a block, transactions are typically ordered with the highest fees at the top, but every now and again opportunities open up that would allow miners to take an additional profit by strategically changing the order of transactions for their own benefit.

You might think, what’s the harm in letting miners take a bit of extra profit off the top? The concerns only start to crop up when some of these miners, those equipped with more advanced analytical capabilities and more powerful computing, can identify and exploit MEV profit opportunities more effectively than others.

These opportunities might not always be easy to spot, but the more value that can be extracted through analyzing the chain, the stronger the incentive becomes for research teams equipped with bots to do this work. Over time, this disparity in miner’s profit-making ability creates a trend toward centralization within the network. Ultimately undermining the core principle of the blockchain: decentralization.

This is exactly the scenario the Bitcoin developer community is aiming to prevent when considering how best to manage more expressivity on Bitcoin.

Historically, Bitcoin has operated with relatively simple smart contracts. However, this model struggles with even moderately complex transactions. Bitcoin Script can only validate authentication data, it doesn’t have the capability to impose speed limits on transactions or define coin destinations because Bitcoin Script doesn’t have access to transaction data.

As a somewhat separate issue, working with and writing Bitcoin smart contracts can be challenging for users who don’t fully grasp its security requirements. A proposed feature, known as ‘vaults,’ aims to solve some of these pain points by introducing time-locked conditions for transactions. Essentially, vaults could serve as an emergency “escape hatch,” allowing users to recover their funds in the event of compromised private keys. But features like this are only possible with more expressivity.

Ethereum is widely recognized for its highly expressive scripting capabilities, but it also notably struggles with the issue of MEV. Most users generally assume that Bitcoin has no MEV, in stark contrast to Ethereum, which is viewed as a wild frontier for it. But is this the full story?

Do more expressive smart contracts automatically incentivize more MEV scenarios?

There are several factors that contribute to MEV: (1) mempool transparency, (2) smart contract transparency, and (3) smart contract expressivity. Each of these factors opens up new channels for MEV, we’ll review each here.

Like Bitcoin’s mempool, the mempools of most blockchains are fully transparent, open, and visible, so that everyone can see what transactions are pending before being validated and confirmed in a block. Bitcoin blocks typically take about 10 minutes to find, which theoretically gives miners that same amount of time to take advantage and front-run.

In practice, on Bitcoin, this isn’t a source of MEV for a few reasons: (1) Bitcoin transactions are simple enough that no miners have a significant analytic advantage over other miners, and (2) Bitcoin transactions generally don’t execute multi-asset transactions such as swaps or open trades that could be front-run.

Contrast this with Ethereum, which has some of the most complex multi-asset transactions taking place on public decentralized exchanges (DEXs). Officially the block time on Ethereum is 15 seconds, but during periods of high mempool traffic, the required gas fees for immediate block inclusion can easily exceed a hundred dollars. As a result, transactions with lower fees end up waiting minutes or even hours before being included in a block. This can extend the window for these nefarious front-running opportunities, already more prevalent on Ethereum due to the substantial value wrapped up in layer-2 tokens.

In Bitcoin “smart contracts” are the simple locking and unlocking mechanism inherent in Bitcoin Script. The transaction values, sender, and receiver details are all publicly visible on the blockchain. While this complete and naked transparency isn’t ideal from a privacy perspective, it’s part of how Bitcoin allows all participants in the network to verify the full state of the blockchain. Any observer can analyze these contract details, potentially opening the door to certain MEV-related strategies.

But the Bitcoin scripting language is, by design, quite limited, focusing primarily on the basic functions of sending and receiving funds, and validating transactions with signatures or hashlocks. This simplicity inherently limits the scope for MEV strategies on Bitcoin, making such opportunities relatively scarce compared to other chains.

Platforms like Ethereum, Solana, and Cardano also have fully transparent smart contracts, but they diverge from Bitcoin by also having highly complex and expressive scripting languages. Their Turing-complete systems make it possible to theoretically execute virtually any computational task which has come to include: self-executing contracts, integration of real-world data through oracles, decentralized applications (dApps), layer-2 tokens, swaps within DEXs, and automated market makers (AMMs). These come together to foster a rich environment for MEV opportunities. Zero-knowledge-proof-based schemes, such as STARKex, could theoretically avoid some of these issues, but this trade-off would come with other complexities.

The MEV opportunities are so lucrative on some chains that there are “MEV trading firms” bringing in “high five figures, mid six figures” in profits a month. This trend has become so prominent that there are public dashboards dedicated to scanning for profitable opportunities on Ethereum and Solana. Their profitability is generated by executing the full basket of MEV strategies: front-running, sandwich trading, token arbitrage, back-running, and liquidations to name a few. Each exploiting a different smart contract dynamics for profit.

Some of these MEV strategies apply to both layer-1 and layer-2.

Generalized Front-Running: Bots scan the mempool for profitable transactions, and then front-run the original transaction for a profit.Sandwich Trading: The attacker places orders both before and after a large transaction to manipulate asset prices for profit. This strategy leverages the predictable price movement caused by the large transaction.

Then certain strategies are unique to layer-2 tokens and smart contracts.

Arbitrage Across Different DEXs: Bots exploit price differences for the same asset on various DEXs by buying low on one and selling high on another.Back-running in DeFi Bonding Curves: MEV bots capitalize on predictable price rises in DeFi bonding curves by placing transactions immediately after large ones, buying during uptrends, and selling for profit. DeFi Liquidations: MEV bots spot opportunities in DeFi lending where collateral values fall below set thresholds, allowing validator’s to prioritize their transactions for buying the liquidated collateral at lower prices.

The complexity of contracts significantly contributes to the challenges associated with MEV.

Re-entrancy Attacks: These attacks exploit smart contract logic flaws, allowing attackers to repeatedly call a function before the first execution completes, extracting funds multiple times. In the context of MEV, skilled individuals can significantly profit from this, particularly in contracts with substantial funds.Interconnected Contracts and Global State: On platforms like Ethereum, smart contracts can interact, leading to chain reactions across several contracts from a single transaction. This interconnectivity enables complex MEV strategies, where a transaction in one contract may impact another, offering a chain reaction of profit opportunities.

Part of the problem here is that the total value created by tokens and dApps built on layer-2 often exceeds the value of the blockchain’s native asset on layer-1, undermining the validators incentive to select and confirm transactions purely based on fees.

To make matters worse, many of these opportunities are not strictly limited to network validators. Other network participants with MEV scanning bots can compete for these same opportunities, causing network congestion, raising gas fees, and elevating transaction costs. This scenario creates a negative externality for the network and its users, who are all affected by the price of higher transaction fees, as the chain becomes less efficient and more expensive to operate. MEV in DeFi is so common that users have almost accepted it as an invisible tax on everyone in the network.

Do these MEV opportunities naturally emerge as a byproduct of the highly expressive smart contracts, or is there an alternative route to the dream of fully programmable money?

Short of avoiding protocols with highly expressive smart contracts and layer-2 tokens, users can avoid some of these risks by utilizing protocols that support Confidential Transactions, like Liquid, that conceal transaction details. But unlike these platforms with more expressive scripting languages, Bitcoin lacks the ability to do things you would expect to be able to do with programmable money.

When considering the evolution of smart contracts on Bitcoin the options we’re given are to (1) push the complexity off-chain, (2) cautiously integrate narrow or limited covenant functionalities, or (3) embrace the path of full expressivity. Let’s explore some of the proposals from each of these options.

Off-chain solutions, like the Lightning Network, aim to enhance Bitcoin’s scalability and functionality without burdening the mainchain, keeping transactions fast and fees low. This all sounds good so far.

SIGHASH_ANYPREVOUT (APO) is a proposal for a new type of public key that allows certain adjustments to a transaction even after it’s signed. It simplifies how transactions are updated, allowing transactions to refer to previous (UTXOs) more easily, making Lightning Network channels faster, cheaper, safer, and more straightforward, especially in resolving disputes.

Under the hood, APO is a new proposed type of sighash flag. Every Bitcoin transaction must have a signature to prove it’s legitimate. When creating this signature, you use a “sighash flag” to determine which parts of the transaction you’re signing. With APO a sender would sign all outputs and none of the inputs, to commit the outputs of the transaction, but not specifically which transaction the funds are going to come from.

APO enables Eltoo, allowing users to exchange pre-signed transactions off-chain. However APO may inadvertently introduce MEV by making transactions reorderable. As soon as you allow a signature that’s binding the transaction graph you have the ability to swap out transactions. Inputs can be swapped, as long as the new inputs are still compatible with the signature.

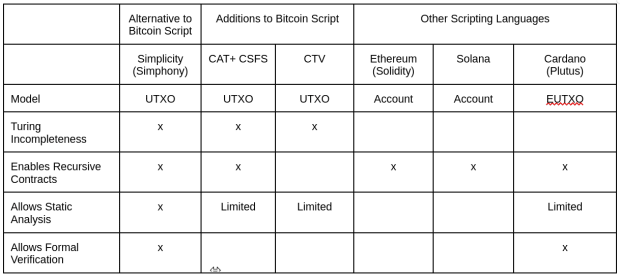

Covenants would allow users to control where coins can move, by imposing speed limits or setting specific destinations for coins in a transaction. There are two different categories of covenants: recursive and non-recursive.

Recursive covenants allow coins to continually return to covenants of the same type.Non-recursive covenants limit this control to the next transaction, requiring the entire future path of the coins to be defined upfront.

CAT + CSFS is a covenant proposal that allows scripts to construct or define certain parts of a future transaction. CHECKSIGFROMSTACK (CSFS) verifies a signature against the data that OP_CAT constructed. By using CSFS to require the signature to match some dynamically constructed format from OP_CAT, we can define how these UTXOs can be spent in the future and create a recursive covenant, albeit clunkily.

OP_CHECKTEMPLATEVERIFY (CTV) is a way of creating non-recursive covenants. Instead of defining and verifying against specific parts of a transaction, CTV restricts how funds can be spent, without specifying the exact next address they must go to. It defines a “template” that the next transaction has to confirm.

One risk with recursive covenants might be possible to create a scenario where coins must follow a set of rules that repeat over and over, that get trapped in a loop without a way of getting out. Another is that, because covenants are transparent and self-executing they could open Bitcoin up to some of the MEV strategies we see on other chains.

What is the good news here?

The good news is that these proposals all introduce new expressivity!

Now what is the maximum amount of expressivity we can get?

Simplicity is a blockchain-based programming language that differs from other scripting languages in that it is very low-level. It is not a language on top of Bitcoin Script or a new opcode within it, it’s an alternative to it. Theoretically, it’s possible to implement all covenant proposals within Simplicity, and implement many of the other contracts cypherpunks want from programmable money, but with less of the negative externalities of Ethereum.

Simplicity maintains Bitcoin’s design principle of self-contained transactions whereby programs do not have access to any information outside the transaction. Designed for both maximal expressiveness and safety, Simplicity supports formal verification and static analysis, giving users more reliable smart contracts.

Compare Simplicity to: (1) bitcoin covenant proposals and (2) scripting languages on other blockchains:

The covenant proposals on Bitcoin Script, though much simpler than Simplicity, lack the expressivity to handle fee estimation in Script, due to Bitcoin’s lack of arithmetic functions. There is no way to multiply or divide, no conditionals or stack manipulations opcodes; it is also very hard to estimate a reasonable fee to be associated with a given contract or covenant. Users end up with spaghetti code, where 80% of their contract logic is dedicated to trying to determine what their fee rate should be. Making these covenant contracts super complicated and difficult to reason about.

The EVM has looping constructs which makes static analysis of gas usage very difficult. Whereas with Script or Simplicity, you can just count each opcode, or recursively add up the cost of each function. Because Simplicity has a formal model, you can formally reason about program behavior. You can’t do this with Script even though you can do static analysis of resource usage.

Simplicity would provide users with the highest degree of expressiveness, along with other valuable features like static analysis and formal verification. Users are incentivized, though not restricted, to build smart contracts that are resistant to MEV. Additionally, a combination of different contracts together may give rise to MEV, even when individually they do not. This represents a fundamental trade-off.

The idea of advancing Bitcoin’s smart contract functionality is undeniably promising and exciting. But it’s important to acknowledge that all these proposals carry some degree of MEV risk—albeit likely not to the extent that we see on other chains. As we think about bringing more programmable money to Bitcoin, there are questions we have to ask:

Can we build a protocol with zero MEV risk, or is this an unattainable ideal?Given the inherent risks of MEV in many proposals, what level of MEV risk is acceptable?And finally, what represents the simplest proposal that offers the greatest degree of expressivity?

Each proposal has its own set of advantages and disadvantages. However, regardless of the direction we take, we should always aim to prioritize security and uphold the principle of decentralization.

For detailed updates and more information, keep an eye on the Blockstream Research 𝕏 feed.

This is a guest post by Kiara Bickers. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

The fourth Bitcoin halving is almost upon us, and this one has the potential for some very interesting surprises. This halving marks the reduction of the Bitcoin supply subsidy from 6.25 BTC every block to 3.125 BTC per block. These supply reductions occur every 210,000 blocks, or roughly every four years, as part of Bitcoin’s gradual, disinflationary approach to its final capped supply in circulation.

The finite supply of 21 million coins is a, if not the, foundational characteristic of Bitcoin. This predictability of supply and inflation rate has been at the heart of what has driven demand and belief in bitcoin as a superior form of money. The regular supply halving is the mechanism by which that finite supply is ultimately enacted.

The halvings over time are the driver behind one of the most fundamental shifts of Bitcoin incentives in the long term: the move from miners being funded by newly issued coins from the coinbase subsidy — the block reward — to being funded dominantly by the transaction fee revenue from users moving bitcoin on-chain.

As Satoshi said in Section 6 (Incentives) of the whitepaper:

“The incentive can also be funded with transaction fees. If the output value of a transaction is less than its input value, the difference is a transaction fee that is added to the incentive value of the block containing the transaction. Once a predetermined number of coins have entered circulation, the incentive can transition entirely to transaction fees and be completely inflation free.”

Historically the halving has correlated with a massive appreciation in the price of bitcoin, offsetting the impact of the miners’ subsidy being cut in half. Miners’ bills are paid in fiat, meaning that if the price of bitcoin appreciates, resulting in a larger income in dollar terms for the lower amount of bitcoin earned per block, the negative impact on mining operation is cushioned.

In light of the last market cycle, with not even a 4x appreciation from the prior all time high, the degree to which price appreciation will cushion miners from the effects of the halving is an assumption that might not consistently hold true. This coming halving, the inflation rate of bitcoin will drop for the first time below 1%. If the next market cycle plays out similarly to the previous one, with much lower upwards movement than seen historically, this halving could have a materially negative impact on existing miners.

This makes the fee revenue miners can collect from transactions more important than ever, and it will continue to become more central to their sustainability from a business perspective as block height increases and successive halvings occur. Either fee revenue has to increase, or the price needs to appreciate at a minimum by 2x each halving in order to make up for the decrease in subsidy revenue. As bullish as most Bitcoiners can be, the notion that a doubling in price is guaranteed to happen every four years, in perpetuity, is a dubious assumption at best.

Love them or hate them, BRC-20 tokens and Inscriptions have shifted the entire dynamic of the mempool, pushing fees from somewhere in the ballpark of 0.1-0.2 BTC per block prior to their existence, to the somewhat volatile average of 1-2 BTC as of late — regularly spiking far in excess of that.

Ordinals present a very new incentive dynamic to the halving this go around that was not present at any prior halving in Bitcoin’s history. Rare sats. At the heart of Ordinals Theory is that satoshis from specific blocks can be tracked and “owned” based on its arbitrary interpretation of the transaction history of the blockchain, based on assuming specific amounts sent to specific outputs “send that sat” there. The other aspect of the theory is assigning rarity values to specific sats. Each block has a coinbase, thus producing an ordinal. But each block is different in importance to the scheme. Each normal block produces an “uncommon” sat, the first block of each difficulty adjustment produces a “rare” sat, and the first block of each halving cycle produces an “epic” sat.

This halving will be the first one since the widespread adoption of Ordinal Theory by a subset of Bitcoin users. There has never been the production of an “epic” sat while there was material market demand for it from a large and developed ecosystem. The market demand for that specific sat could wind up being valued at absurd multiples of what the coinbase reward itself is valued at in terms of just fungible satoshis.

The fact that a large market segment in the Bitcoin space would value that single coinbase drastically higher than any other creates an incentive for miners to fight over it by reorganizing the blockchain immediately after the halving. The only time such a thing has happened in history was during the very first halving, when the block reward decreased from 50 BTC to 25 BTC. Some miners continued trying to mine blocks rewarding 50 BTC in the coinbase after the supply cut, and gave up shortly after when the rest of the network ignored their efforts. This time around, the incentive to reorg isn’t based around ignoring the consensus rules and hoping people come along to your side, it’s fighting over who is allowed to mine a completely valid block because of the value collectors will ascribe to that single coinbase.

There are no guarantees that such a reorg will actually occur, but there is a very large financial incentive for miners to do so. If it does occur, the length for which it will go on ultimately depends on how much that “epic” sat could be worth on the market to pay for the lost revenue from fighting over a single block rather than progressing the chain.

Each halving in Bitcoin’s history has been a pivotal event people watch, but this go around it has the potential to be much more interesting than past halvings.

There are a few ways this could play out in my opinion. The first and most obvious way is that nothing happens. For whatever reason, miners do not judge that the potential market value of the first “epic” sat mined since Ordinals adoption took off is worth the opportunity cost of wasting energy reorging the blockchain and foregoing the money they could make by simply mining the next block. If miners do not think the extra premium the ordinal can fetch is worth the cost of giving up moving on to the next block, they simply won’t do it.

The next possibility is a result of nuanced scales of economy. Imagine a larger scale mining operation can afford to risk more “lost blocks” engaging in a reorg fight over the “epic” sat. That larger miner with more capital to put on the table can afford to take a larger risk. In this scenario, we might see a few odd reorg attempts by larger miners with smaller operations not even trying, and essentially minimal disruption. This would play out if miners think there is some premium they can acquire for the ordinal, but not a massive premium worth serious disruption to the network.

The last scenario would be if a market develops bidding for the “epic” sat ahead of time, and miners can have a clear picture that the ordinal is valued massively above the market value of the fungible sat itself. In this case, miners may fight over that block for an extended period of time. The logic behind not reorging the blockchain is that you are losing money, you are not only forgoing the reward of just mining the next block, but you are also continuing to incur the cost of running your mining operations. In a situation where the market is publicly signaling how much the “epic” sat is worth, miners have a very clear idea of how long they can forgo moving onto the next block and still wind up with a net profit by attaining the post-halving coinbase reward with the ordinal. In this scenario the network could see substantial disruption until miners begin approaching the point of incurring a guaranteed loss even if they do successfully wind up mining this block without it being reorged.

Regardless of which way things actually play out, this is going to be a factor to consider each halving going forward unless the demand and marketplace for ordinals dies off.

In a move to catalyze the growth within the Bitcoin ecosystem, Ego Death Capital announces the launch of a new funding round, Fund II, aiming to raise $100 million. Founded in 2021, the venture capital firm, led by Jeff Booth, Andi Pitt, Nico Lechuga, with advisory support from Preston Pysh, Lyn Alden, and Pablo Fernandez, has successfully initiated Fund II with a focus on investing in companies driving Bitcoin’s acceleration.

“A parallel system bringing truth, hope, and abundance to our world is growing much faster than people realize and we feel super fortunate to be a part of it,” said founding partner Jeff Booth.

Fund I, which raised $25.2 million, demonstrated the foresight of ego death capital in recognizing Bitcoin’s emergence not just as a store of value but as a foundational layer for a new peer-to-peer decentralized internet tied to energy. The success of their initial fund was marked by strategic investments in companies like Fedi, Breez, Synota, Relai, and Wolf.